Why DSCR Loans Are the Preferred Financing Strategy for LLC Real Estate Investors in 2026

In 2026, real estate investors are no longer winning with the cheapest capital alone. They’re winning with execution speed, underwriting flexibility, and financing that matches how investment businesses actually operate.

That shift is exactly why DSCR loans for LLC real estate investors continue to gain traction.

After several years of elevated borrowing costs, tighter bank credit, and more disciplined deal selection, seasoned investors have adjusted. The focus is now on cash flow, margin protection, and scalable financing structures—not on forcing investment-property deals through conventional underwriting built for owner-occupied borrowers.

For investors acquiring or refinancing rental properties through an LLC, DSCR financing has become one of the most practical tools in the market.

2026 Market Conditions Still Favor Cash-Flow-Based Lending

The financing environment in 2026 continues to reward investors who can move decisively on income-producing assets.

Traditional lenders are still selective. Conventional underwriting still creates friction. And for experienced investors with multiple properties, layered entities, aggressive depreciation, or complex tax returns, personal-income documentation often tells the wrong story.

That’s where DSCR loans stand out.

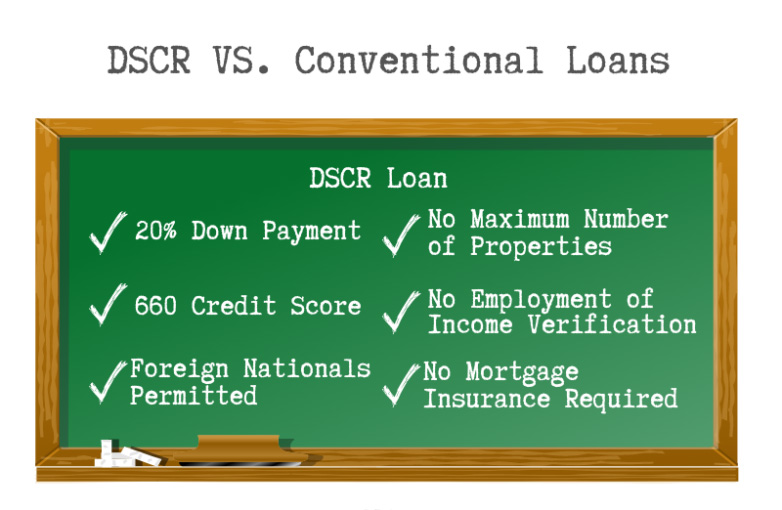

Instead of centering the underwriting decision around personal W-2 income or tax-return cash flow, DSCR financing focuses primarily on the property’s ability to support the debt. For professional investors, that is a major advantage.

In other words, the market is favoring financing that evaluates the asset like an investment—not the borrower like a salaried employee.

Why LLC Real Estate Investors Are Leaning Harder Into DSCR Loans

For serious operators, buying in an LLC is standard practice.

LLC ownership can support:

- cleaner entity-level bookkeeping

- better asset segregation

- more efficient portfolio management

- partnership structuring

- operational consistency across multiple properties

That makes DSCR loans for LLC real estate investors especially attractive. Many investor-focused lenders allow title to be held in the LLC, even when a personal guaranty is still part of the structure.

That matters because sophisticated investors are not just buying one property. They are building a business. And financing needs to align with that reality.

In 2026, more investors are prioritizing entity-based lending solutions that support scale without forcing every transaction through full personal-income underwriting.

The Strategic Advantages of DSCR Loans in 2026

1. Qualification Is Tied to Property Performance

One of the biggest reasons DSCR loans remain competitive is simple: they underwrite the deal based on rental income.

For investors with legitimate write-offs, depreciation-heavy returns, or uneven taxable income, that is a far better fit than conventional loan programs that may understate real borrowing strength.

If the property cash flows, the loan becomes much easier to structure.

2. Faster Closings Create a Real Competitive Edge

In a market where good deals still move quickly, speed matters.

DSCR lenders are often better positioned to move efficiently on:

- acquisitions

- rate-and-term refinances

- cash-out refinances

- portfolio expansion strategies

For investors competing on time-sensitive opportunities, closing certainty can matter as much as rate.

3. DSCR Loans Support Portfolio Growth

Conventional financing tends to become more cumbersome as investors add doors, entities, and financing relationships. DSCR lending can provide a more scalable path for investors who are actively growing a rental portfolio.

That’s especially relevant for borrowers operating in the $500K to $10M deal mindset, where the focus is less about one-off transactions and more about repeatable capital strategy.

4. LLC Borrowing Keeps the Structure Cleaner

When properties are acquired and managed through business entities, financing needs to work with that structure—not against it.

DSCR loans can help investors maintain cleaner operational alignment between ownership, management, accounting, and long-term portfolio strategy.

What Lenders Are Really Looking at in 2026

Even though DSCR loans are more flexible than conventional mortgages, experienced investors know they are not “easy money.”

In 2026, lenders are still paying close attention to the fundamentals, including:

- Debt service coverage ratio (DSCR): Does the rental income support the proposed payment?

- Loan-to-value (LTV): How much leverage is being requested?

- Rent strength: Are in-place rents or market rents solid and defensible?

- Credit profile: Is the borrower financially stable and experienced?

- Liquidity and reserves: Does the borrower have enough cushion post-close?

- Property condition and occupancy: Is the asset stable and financeable?

Strong borrowers still get rewarded—but only when the deal pencils.

Where DSCR Financing Makes the Most Sense for Investors

For LLC real estate investors, DSCR loans are especially compelling in a few common scenarios.

Stabilized Rental Acquisitions

When an investor is buying a cash-flowing property and wants the underwriting tied to the asset—not personal tax returns—DSCR is often the cleanest solution.

Refinancing Out of Short-Term Capital

Many investors use bridge or rehab financing to reposition a property, then refinance into a longer-term DSCR loan once rents are stabilized.

Cash-Out Refinance to Recycle Equity

In a market where liquidity and optionality matter, a DSCR cash-out refinance can help investors redeploy trapped equity into the next acquisition.

Portfolio Expansion Through LLCs

For investors growing deliberately, DSCR financing can make it easier to add properties without creating unnecessary underwriting drag every time a new deal hits the pipeline.

What Sophisticated Investors Should Watch Before Signing a Term Sheet

The strongest borrowers in 2026 are not just comparing rates. They are comparing structure.

Before choosing a DSCR loan, experienced investors should closely evaluate:

- Prepayment penalties

- Interest-only options

- Reserve requirements

- Cash-out seasoning rules

- Appraisal methodology

- Rent treatment

- Lender execution history

- Extension and refinance flexibility

A low headline rate means very little if the loan structure limits your exit, kills your refinance window, or compresses future cash flow.

This is where investor-grade underwriting matters. The best financing strategy is the one that protects the full business plan—not just the closing date.

Bottom Line

In 2026, DSCR loans are no longer a niche workaround. They are a strategic financing solution for LLC real estate investors who care about speed, scalability, and cash-flow-based decision-making.

For investors building and refinancing rental portfolios, the appeal is clear:

- less friction than conventional underwriting

- better alignment with entity ownership

- faster execution

- financing based on property economics

When the asset is strong and the loan structure is right, DSCR financing can be one of the most effective ways to acquire, refinance, and scale investment real estate in today’s market.

If you’re financing rental property through an LLC in 2026, don’t just compare interest rates. Compare DSCR thresholds, leverage, reserves, prepay structure, and closing certainty—because sophisticated investors know the loan terms can shape the deal just as much as the purchase price.