Explained | Construction Loans

Ground-Up Construction Loans: Building Your Vision From the Foundation Up

Ground-Up Construction Loans: Building Your Vision From the Foundation Up

What Is a Ground-Up Construction Loan?

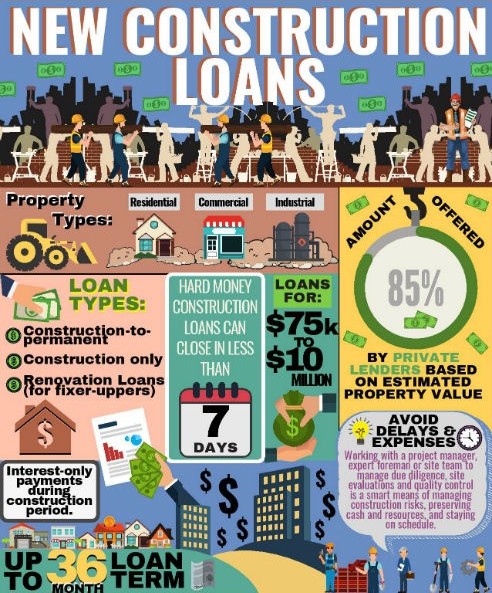

A Ground-Up Construction Loan is a specialized financing solution designed for developers, builders, and real estate investors who are constructing a brand new structure on raw or cleared land — starting entirely from scratch. Unlike Fix & Flip or renovation loans that work with an existing structure, ground-up construction financing funds the complete building process from land acquisition and site preparation all the way through to a finished, market-ready property.

These loans are purpose-built for projects where no habitable structure currently exists, including:

- Vacant or raw land

- Lots where an existing structure has been or will be demolished

- Subdivided parcels ready for new development

The Core Concept: Acquire the land → Finance the construction → Complete the build → Sell, rent, or refinance the finished property into permanent financing.

Ground-Up Construction Loans are short-term, asset-based financing instruments that fund the project in stages, releasing capital as construction milestones are reached and verified — ensuring both the lender and the borrower stay aligned throughout the entire build process.

How Do Ground-Up Construction Loans Work? The Qualification Process

Ground-Up Construction Loans have a more detailed underwriting process than Fix & Flip loans, reflecting the greater complexity and longer timeline of building from scratch. Here’s how the process typically works:

1. 🗺️ Project & Site Evaluation

Before anything else, the lender evaluates the land and the overall feasibility of the project. Key considerations include:

- Land Value & Ownership — whether the borrower already owns the land or is acquiring it simultaneously

- Zoning & Entitlements — confirmation that the land is properly zoned for the intended use

- Utilities & Infrastructure — access to water, sewer, electrical, and road access

- Market Demand — analysis of the local real estate market and demand for the planned property type

- Environmental Considerations — any potential soil, wetland, or environmental concerns

2. 📋 Complete Project Documentation

Ground-Up loans require a comprehensive project package submitted to the lender, which typically includes:

- Architectural plans and blueprints

- Engineered site plans and surveys

- Building permits (or confirmation they are in process)

- A detailed construction budget and cost breakdown

- A project timeline with construction milestones

- General contractor information, credentials, and license verification

3. 📐 Key Lending Metrics

Lenders evaluate ground-up construction loans using several critical ratios:

| Metric | What It Measures | Typical Range |

|---|---|---|

| LTC (Loan-to-Cost) | Loan amount vs. total project cost | Up to 80–85% |

| LTV / ARV (After Repair Value) | Loan amount vs. completed property value | Up to 65–75% of ARV |

| Loan-to-Land Value | Loan vs. current land value | Varies by program |

Example: If your total project cost is $1,000,000 and the completed property’s ARV is $1,500,000, a lender offering 80% LTC and 70% ARV would cap the loan at $800,000 based on cost and $1,050,000 based on ARV — the lower of the two figures typically governs.

4. 🏗️ Construction Draw Schedule

Funds are never disbursed all at once. Instead, the loan is structured around a carefully planned draw schedule tied to verified construction milestones. Typical draw stages might include:

- Draw 1 — Foundation complete

- Draw 2 — Framing complete

- Draw 3 — Mechanical, electrical & plumbing (MEP) rough-in complete

- Draw 4 — Drywall, roofing & exterior complete

- Draw 5 — Interior finishes, fixtures & final completion

Each draw is triggered by a third-party inspection confirming that the prior phase of work has been satisfactorily completed before the next round of funds is released.

5. ✅ Borrower Qualification Factors

While the project and its numbers are the primary focus, lenders will also evaluate:

- Credit Score — typically 620–680 minimum, though stronger profiles unlock better terms

- Real Estate & Development Experience — prior ground-up construction experience is highly valued and can significantly influence loan terms

- Financial Strength & Liquidity — ability to cover cost overruns, carrying costs, and project contingencies

- Down Payment / Equity Injection — typically 15–25% of total project cost

- General Contractor Qualifications — lenders want to see a licensed, experienced, and financially stable GC leading the build

- Contingency Reserves — most lenders require a 10–15% contingency budget built into the project to cover unexpected costs

- Exit Strategy — a clear and credible plan for loan repayment upon project completion (sale, refinance, or lease-up)

6. 📅 Loan Terms & Structure

Ground-Up Construction Loans are structured as short-to-medium term financing:

- Loan Terms typically range from 12 to 24 months, with extensions available for larger or more complex projects

- Interest is generally charged only on drawn funds, not the full loan commitment — helping manage carrying costs during the build

- Interest Reserves can sometimes be built into the loan, deferring interest payments until construction is complete

- Upon project completion, borrowers typically refinance into permanent financing such as a DSCR loan, commercial mortgage, or conventional loan

7. ⚡ Speed & Flexibility Compared to Bank Financing

Traditional bank construction loans involve lengthy approval timelines, rigid underwriting, and extensive personal financial documentation. Private and alternative ground-up construction lenders offer:

- Faster approvals — often 2 to 4 weeks

- More flexible underwriting focused on the deal’s merit

- Financing for borrower types banks won’t touch — including self-employed developers, foreign nationals, and newer investors with strong projects

Ideal Situations for Ground-Up Construction Loans

Ground-Up Construction financing serves a wide range of development strategies and property types. Here are the most common and profitable scenarios:

🏠 Single-Family Residential New Construction

Builders and investors developing new single-family homes on vacant lots — whether for sale to end buyers or to hold as rental properties — are among the most common users of ground-up construction financing. This includes everything from entry-level starter homes to luxury custom builds.

🏘️ Residential Subdivision Development

Developers acquiring larger parcels of land and subdividing them into multiple residential lots for sequential home construction can use ground-up construction loans to fund individual builds or phase the development across multiple loan draws and projects.

🏢 Multi-Family & Apartment Development

Investors and developers constructing duplexes, fourplexes, townhome communities, or larger apartment complexes are ideal candidates for ground-up construction financing — particularly when the project is designed to be held as a long-term income-producing asset and refinanced into permanent debt upon stabilization.

🛍️ Commercial & Retail Development

Ground-Up loans are widely used in the development of commercial real estate — including retail strip centers, office buildings, medical facilities, self-storage facilities, and industrial properties — where a developer is building to suit a tenant, a portfolio, or a future sale.

🏨 Hospitality & Short-Term Rental Developments

Developers constructing boutique hotels, extended stay properties, or short-term rental communities (such as cabin resorts or glamping developments) can leverage ground-up financing to bring these high-yield hospitality concepts to life.

🏗️ Infill Development Projects

Infill development — building on vacant or underutilized lots within established urban or suburban neighborhoods — is one of the highest-demand uses for ground-up construction loans. These projects capitalize on existing infrastructure and strong market demand while adding housing supply to land-constrained markets.

🌿 Teardown & Rebuild Projects

When an existing structure is beyond the point of cost-effective renovation, developers opt to demolish and rebuild entirely. Ground-up construction loans can fund both the demolition and the complete rebuild, maximizing the land’s highest and best use.

🏡 Custom Home Builder Programs

Licensed spec home builders who consistently develop new construction properties for resale use ground-up construction loans as their primary business financing tool — cycling through projects with short-term construction capital and repaying upon each home sale.

🌆 Mixed-Use Development

Developers building properties that combine residential units with ground-floor commercial space — a growing and highly desirable asset class in urban markets — can finance these complex projects through ground-up construction lending tailored to mixed-use development.

The Ground-Up Construction Loan Process at a Glance

STEP 1: Initial Consultation & Project Review

↓

STEP 2: Submit Project Package (Plans, Budget, Timeline, GC Info)

↓

STEP 3: Lender Underwriting & Third-Party Appraisal (ARV)

↓

STEP 4: Loan Approval & Term Sheet Issued

↓

STEP 5: Closing & Initial Land / Mobilization Draw

↓

STEP 6: Construction Begins — Draw Requests & Inspections

↓

STEP 7: Project Completion & Certificate of Occupancy

↓

STEP 8: Exit — Sell, Rent & Refinance, or Permanent Financing

Ground-Up Construction vs. Other Loan Types

| Feature | Ground-Up Construction | Fix & Flip | Conventional Mortgage |

|---|---|---|---|

| Property Condition | Vacant Land / New Build | Existing Structure | Move-In Ready |

| Loan Purpose | Build From Scratch | Renovate & Sell | Purchase or Refinance |

| Loan Term | 12–24 Months | 6–18 Months | 15–30 Years |

| Fund Disbursement | Draw Schedule | Draw Schedule | Lump Sum |

| Income Verification | Minimal | Minimal | Extensive |

| Approval Speed | 2–4 Weeks | 1–2 Weeks | 30–60 Days |

| Experience Required | Preferred | Helpful | Not Required |

| Exit Strategy Required | ✅ Yes | ✅ Yes | ❌ No |

Ready to Break Ground on Your Next Project?

Whether you’re a seasoned developer with a track record of successful builds or an ambitious investor ready to take on your first ground-up project, our construction lending team has the expertise and the capital to help you bring your vision to life — from the first shovel in the ground to the final certificate of occupancy.

Start Your Project Consultation Today and let our specialists structure a ground-up construction loan that fits your timeline, your budget, and your investment goals.